Are HSBC shares a FTSE bargain? Here’s what the charts say!

There are plenty of dirt-cheap FTSE 100 banking stocks for investors to choose from today. Our writer Royston Wild believes HSBC could be the greatest. The post Are HSBC shares a FTSE bargain? Here’s what the charts say! appeared first on The Motley Fool UK.

The FTSE 100 is packed with brilliant value shares right now. The UK’s premier share index has recovered ground from the lows of late 2022. But many top stocks continue to trade well below their true value.

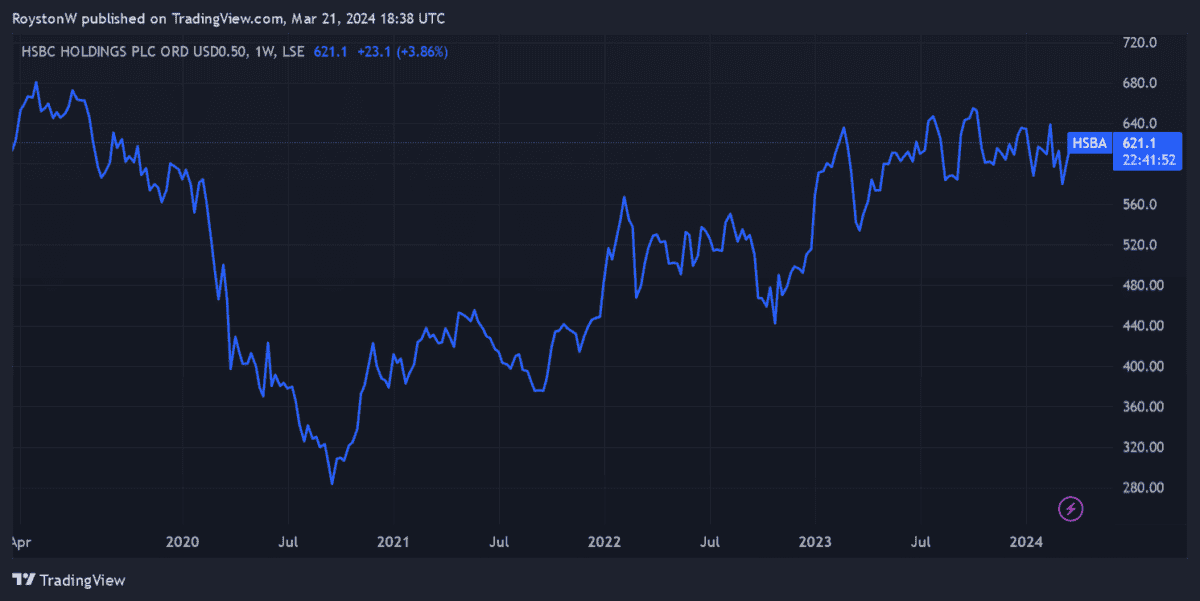

Take HSBC Holdings (LSE:HSBA) for instance. In my opinion it’s the Footsie’s greatest banking stock to buy at current prices. Let me show you why.

Earnings

The first thing to look at is how cheap the bank’s shares are in relation to the value of its earnings. At 621p per share, it trades on an historical price-to-earnings (P/E) ratio of just 6.7 times. This is well below the FTSE 100 average of 11 times.

As the table below shows, this figure is also in and around the forward earnings multiples of Lloyds and Barclays. Fellow emerging market bank Standard Chartered is more expensive on this metric, while NatWest is the best priced.

Bank

P/E ratio

Lloyds Banking Group

6.6 times

Barclays

6.5 times

NatWest Group

4.9 times

Standard Chartered

7.9 times

The average P/E ratio for all five firms sits at 6.5, meaning HSBC trades at a fractional premium to the group.

Dividends

The dividend yield is another useful way to assess the bank’s value. This expresses dividend income as a percentage of the current share price.

Today, HSBC’s historical yield comes in at 7.9%. By comparision, the wider FTSE 100 average sits way back at 3.7%.

And as the table illustrates, HSBC’s yield smashes each of those of its Footsie peers on this metric. It’s a full percentage point ahead of second-placed NatWest’s yield. It’s also well above the group’s average of 5.5%.

Bank

Dividend yield

Lloyds Banking Group

5%

Barclays

4.7%

NatWest Group

6.9%

Standard Chartered

3.2%

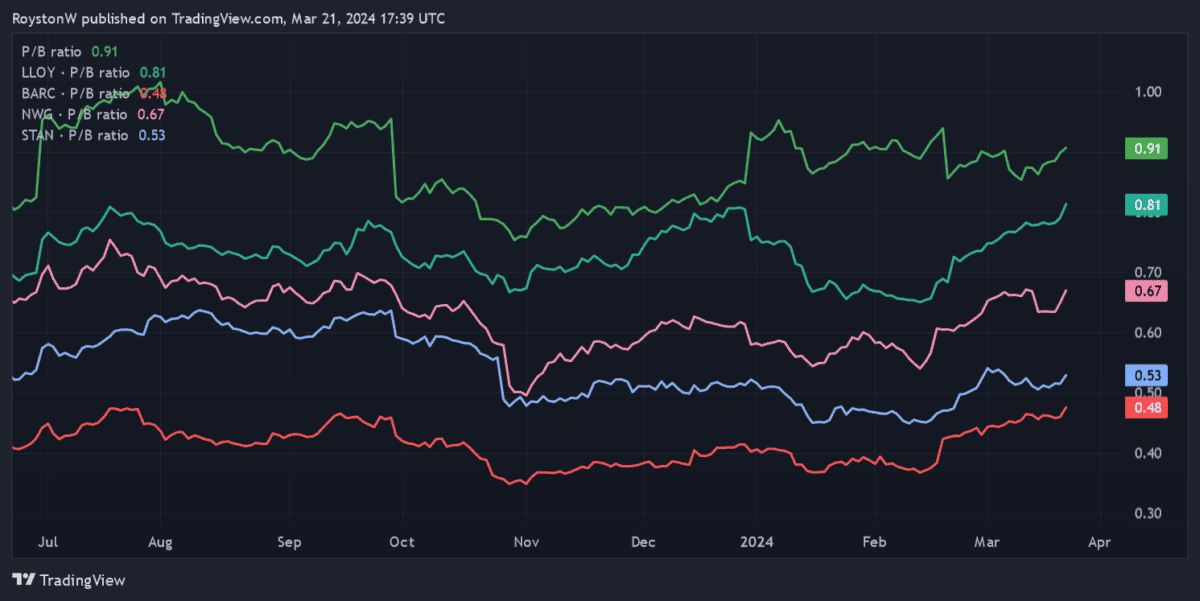

Assets

The final thing to look at is how HSBC shares are valued relative to the company’s assets. One way to do this is to consider its price-to-book (P/B) value, which divides the total book value (assets minus liabilities) by the total number of shares outstanding.

As we can see, HSBC shares trade on a higher P/B value than each of the FTSE 100’s other major banks. At 0.91, its ratio is almost twice as great as that of Barclays.

Having said that, the bank still looks dirt cheap using this metric. Any reading below 1 suggests a company’s trading below the value of its assets.

The verdict

On reflection, HSBC doesn’t look incredibly cheap compared to its peers. Indeed, it only really looks like a standout value share when it comes to dividend yield.

But all things considered, it still seems to offer excellent value when looking at earnings, dividends and assets. And I’d certainly rather buy it than any of those other FTSE banks.

HSBC does face some uncertainty over the short term as China’s economy splutters. But the long-term outlook for the country and wider region — and, by extension, for the bank — remains outstanding.

Banking product penetration in its emerging markets remains extremely low. And as population levels and personal incomes there steadily rise, HSBC has an excellent chance to grow profits.

I think it’s one of the best FTSE 100 value shares to consider buying today.

The post Are HSBC shares a FTSE bargain? Here’s what the charts say! appeared first on The Motley Fool UK.

Should you buy HSBC now?

Don’t make any big decisions yet.

Because Mark Rogers — The Motley Fool UK’s Director of Investing — has revealed 5 Shares for the Future of Energy.

And he believes they could bring spectacular returns over the next decade.

Since the war in Ukraine, nations everywhere are scrambling for energy independence,

he says. Meanwhile, they’re hellbent on achieving net zero emissions.

No guarantees, but history shows…

When such enormous changes hit a big industry, informed investors can potentially get rich.

So, with his new report, Mark’s aiming to put more investors in this enviable position.

Click the button below to find out how you can get your hands on the full report now, and as a thank you for your interest, we’ll send you one of the five picks — absolutely free!

setButtonColorDefaults("#5FA85D", 'background', '#5FA85D'); setButtonColorDefaults("#43A24A", 'border-color', '#43A24A'); setButtonColorDefaults("#FFFFFF", 'color', '#FFFFFF'); })()

More reading

- Investing £5 a day could help me build a second income of £329 a month!

- 2 of my top FTSE stocks to consider buying for passive income before April

- With an 8% dividend yield, these 2 undervalued shares are a winning combo

- 3 of the best FTSE 100 and FTSE 250 shares I’d buy before the ISA deadline!

- £7,000 in savings? Here’s how I’d try and turn that into a £1,253 monthly second income

HSBC Holdings is an advertising partner of The Ascent, a Motley Fool company. Royston Wild has no position in any of the shares mentioned. The Motley Fool UK has recommended Barclays Plc, HSBC Holdings, Lloyds Banking Group Plc, and Standard Chartered Plc. Views expressed on the companies mentioned in this article are those of the writer and therefore may differ from the official recommendations we make in our subscription services such as Share Advisor, Hidden Winners and Pro. Here at The Motley Fool we believe that considering a diverse range of insights makes us better investors.

What's Your Reaction?